Mining & Quarrying in the UK

Production

The UK has relatively diverse and large deposits of minerals that have been mined historically.

Key sectors include:

- Construction minerals – aggregates, brick clay and cement raw materials;

- Industrial minerals – kaolin (china clay) and ball clay, silica sand, gypsum, potash, polyhalite, salt, industrial carbonates, fluorspar and barytes; and

- Metal minerals – tungsten, gold.

- Energy minerals – coal;

The largest bulk market for non-energy minerals is construction. Industrial minerals extracted and used in the UK range from those used primarily domestically (for example, silica sand and limestone for glassmaking, iron and steel manufacture) and minerals such as kaolin, ball clay and potash, which have significant international markets. Mineral production supports a wide variety of upstream, midstream and downstream industries.

Cornish Lithium recently reported it has found “globally significant” lithium grades in geothermal waters and is preparing for work on its pilot plant. Cornwall Resources are also moving forward with the development of their Redmoor project, of a significant tin, tungsten and copper deposit and a mining scoping study has recently been completed. The significant resource of gold at Curraghinalt in Northern Ireland (Dalradian) and Cononish in Scotland (Scotgold), where a recent announcement has been made to accelerate plans to double production, are other exciting examples that illustrate the continuing importance of the UK as a mineral producer.The South Crofty project is working towards the reopening of the South Crofty tin mine in Cornwall.

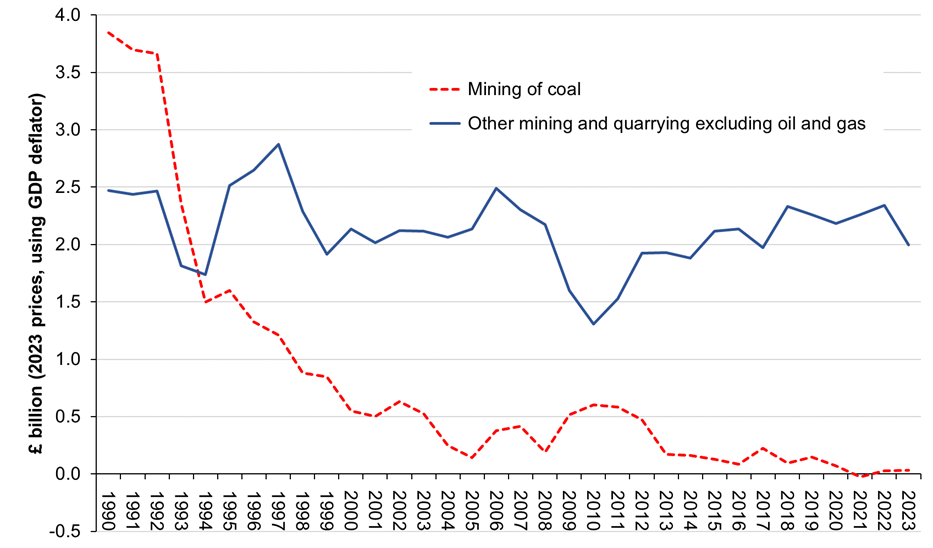

Non-energy UK mining and quarrying has been broadly flat in recent years while coal production volumes have consistently fallen for the past three decades. A planned new coal mine at the Woodhouse Colliery, near Whitehaven, was originally approved to provide metallurgical or coking coal for use in steel production. This decision is now subject to a public inquiry.

Figure 1. Gross Value Added (GVA) of UK mining and quarrying (excluding oil and gas)

Source: ONS, UK GDP(O) low level aggregates, published March 2024

Additional sources of data on mineral production include:

Aggregate minerals survey for England and Wales, 2019 and 2019 Aggregate Minerals Survey for Scotland (published in 2023). These surveys aim to provide comprehensive data for monitoring and facilitating aggregates provision at local, regional and national level.

Annual Minerals Statements (for Northern Ireland); provide volumes and values of minerals produced each year, most recently for 2022.

Profile of the UK Mineral Products Industry and accompanying Statistical Workbook. This report highlights the industry’s significant contribution to the UK economy through the domestic production of construction and industrial mineral products from 2,300 active quarries and plants nationwide.

AMPS 2022 - 10th Annual Mineral Planning Survey [AMPS] Report.

The area involved – 25th annual report: Marine aggregate extraction 2022 provides regional totals for volume of construction aggregate dredged.

Data Sources

Although the UK has significant domestic supply of some minerals, it is a net importer of many minerals and mineral-based products, particularly metals, and in the long term has experienced a balance of trade deficit.

Primary aggregates are largely extracted from indigenous sources and imports are limited, estimated to represent less than 5 million tonnes per annum. Small tonnages of crushed rock, marine sand and gravel, dimension stone and industrial clay are also exported, mainly to Belgium, France and the Netherlands.

The Office for National Statistics (ONS) publishes data on the volume of production and trade of metal ores and non-metallic minerals in its material flows account for the UK while they also report on the value of imports and exports. These data have yet to be verified so they are not included here to avoid giving a misleading impression of the scale of the sector.

The British Geological Survey (BGS) produce a periodic United Kingdom Minerals handbook which includes statistical data on the production of UK mineral resources including construction, industrial and metal minerals.

The Mineral Products Association (MPA) also produces a periodic Profile of the UK Mineral Products Industry - 2023 Edition, which sheds light on the breadth of the minerals and manufactured mineral products industry, from the diversity of the products and their uses, the scale of their markets, to their environmental and sustainability attributes. The MPA also publish their Sustainable Development Reports, which is derived from energy use from different activities.

Additional data sources and methodologies include:

The DESNZ methodologies for calculating production volumes and values for solid fuels and derived gases.

Quality assurance of administrative data report for mining of coal and lignite and extraction of crude petroleum and natural gas industries.

Environmental accounts on material flows QMI (Quality and Methodology Information).

Legal framework

Extraction of minerals is subject to the UK’s mineral planning process. The aim of mineral planning is to facilitate the sustainable supply and use of minerals. Mineral working is not a permanent use of land, and extraction sites are usually restored for beneficial after-use.

Mineral planning policy is devolved and set out in the National Planning Policy Framework (England), Planning Policy Wales and, for Scotland, National Planning Framework 4. In Northern Ireland, policy and guidance are provided through documents such as the Strategic Planning Policy Statement for Northern Ireland, which partly supersedes the Planning Strategy for Rural Northern Ireland. In Northern Ireland since 1 April 2015 responsibility for planning is shared between the Department of the Environment (from 8th May 2016 in respect of planning, the Department of Infrastructure and the eleven local councils).

Exploration for and extraction of metalliferous and industrial minerals are licensed by the Department for the Economy in Northern Ireland under the Mineral Development (Northern Ireland) Act 1969. The UK framework is supported by technical documents providing guidance on particular issues of mineral planning. The focus of the mineral planning process is on whether the development itself is an acceptable use of the land [1].

In England, mineral planning and decisions on planning applications are a responsibility of a local authority body referred to as mineral planning authorities (mpas). In most areas of England, mpas are the County Councils or National Parks Authorities. In Wales and Scotland, Local Planning Authorities including Local Authorities and National Parks Authorities are largely responsible for minerals planning. In Wales and some parts of England the mpa function may be delivered by Unitary Authorities. In Northern Ireland, the Minerals Unit, part of the Planning Service of the Department of the Environment, was responsible for minerals planning until 1 April 2015 [2].

Mpas/local planning authorities have four areas of planning responsibility:

- Planning to guide future developments;

- Safeguarding mineral resources;

- Managing developments by deciding on planning applications; and

- Monitoring and enforcement of existing planning permissions.

Some minerals permissions last for several decades, and where this is the case there may be a need for periodic reviews of the planning conditions attached to that permission. Mpas control mineral developments under the orders established under the Town and Country Planning Act 1990 (Section 97, Part II of Schedule 5, and Schedule 9) [3]. In Scotland, local planning authorities control mineral developments under the Town and Country Planning (Scotland) Act 1997, including Schedule 3.

Minerals extraction may only take place if the operator has the agreement of the landowner and has obtained both a planning permission from the mineral planning authority and any other regulatory permits and approvals. The latter may include:

- Permits relating to borehole construction, surface water, groundwater and mining waste, issued by the Environment Agency, Natural Resources Wales, Northern Ireland Environment Agency or Scottish Environment Protection Agency (under UK devolved legislation related to the EU Water Framework Directive and Mining Waste Directive);

- Marine licences under the Marine and Coastal Access Act 2009 or Marine (Scotland) Act 2010 issued by the relevant regulator: the Marine Management Organisation in England, Natural Resources Wales in Wales, Scottish Government Marine Directorate in Scotland, and the Department of Agriculture, Environment and Rural Affairs in Northern Ireland;

- Where appropriate, European Protected Species Licences, issued by Natural England, Natural Resources Wales or NatureScot. For activities in the marine environment, European Protected Species Licences, for commercial activities, are issued by the Scottish Government Marine Directorate;

- Where appropriate heritage asset consents issued by Historic England, Cadw or Historic Environment Scotland;

- Licences for exploration and extraction of coal, or agreements to enter into or pass through a coal seam to extract any other mineral, need to be granted by the Mining Remediation Authority; and

- Commercial agreements for exploration and extraction of minerals managed by The Crown Estate (TCE) need to be obtained from the latter [4].

In Northern Ireland and Scotland, management of extractive waste is applied through the local planning authority.

Additional consents, such as relating to diverting and reinstating rights of way or temporary road orders, may need to be obtained. Additional rights of way and land use may need to be secured from landowners. Active mining and quarrying operations are also regulated by the Health and Safety Executive (in Great Britain). The corresponding Northern Ireland regulatory authority is the Health and Safety Executive for Northern Ireland (HSENI).

The Control of Major Accident Hazards (COMAH) Regulations limit the consequences to people and the environment of any major accidents involving dangerous substances which occur. COMAH 2015 is enforced by a Competent Authority that comprises the Health and Safety Executive (or the Office for Nuclear Regulation for nuclear establishments), acting jointly with the appropriate environmental agency. In England this is the Environment Agency, in Wales it is Natural Resources Wales, and in Scotland it is the Scottish Environment Protection Agency.

Marine plans are being developed by each of the UK marine planning authorities in accordance with the requirements of the Marine and Coastal Access Act 2009 and the UK Marine Policy Statement. In Scotland, Scottish Ministers are the marine planning authority and marine planning is undertaken in line with the Marine (Scotland) Act 2010 for the inshore region (0 -12 nm), and the UK Marine and Coastal Access Act 2009 for the offshore region (12 – 200 nm).

A marine plan:

- Aims to further the achievement of sustainable development, including the protection and, where appropriate, enhancement of the health of that area, so far as is consistent with the proper exercise of that function.

- Helps marine users understand the best locations for their activities, including where new developments may be appropriate.

Relevant public authorities must take their decisions in accordance with the relevant marine planning documents, i.e. the UK Marine Policy Statement and any marine plan prepared and adopted by the marine planning authority.

Information about mineral planning and environmental permitting within the UK’s devolved administrations is available as follows:

- Scottish Government, Guide to the Planning System in Scotland.

- Scottish Government, guidance on marine licensing and consenting

- Scottish Government, National Marine Plan

- Northern Ireland Environment Agency (NIEA) and Scottish Environment Protection Agency (SEPA), NetRegs website: Environmental Guidance for Your Business in Northern Ireland and Scotland includes guidance on mining and quarrying and managing extractive waste.

- Northern Ireland Planning Service, Minerals Planning.

- Welsh Government, Planning

- Natural Resources Wales, Mining waste.

Mineral ownership and commercial licensing

With the exception of oil, gas, coal, gold and silver, mineral rights in Great Britain [6] vest in landowners rather than the state. It follows that there is no single, national commercial licensing system for the exploration and extraction of such privately owned minerals. While planning permissions and environmental permits are generally required for such purposes, these are not commercial licences.

Where mineral rights belong to a private landowner, permission for exploration must be received from the landowner. As TCE and (in GB) the Forestry Commission manage land on behalf of The Crown, they also issue exploration and extraction licences for mineral deposits under their management and grant access right permits (wayleaves). In some cases, mineral rights can be managed by a private agent on behalf of a public body (TCE and Forestry Commission Scotland).

The MSG does not believe there are any non-trivial deviations in the award or transfer of licences for 2024 or previous years covering marine aggregates, marine licences, terrestrial mining licences, terrestrial mining licences, Northern Ireland licences and any other licences.

Northern Ireland

With certain exceptions, mineral rights in Northern Ireland [7] are vested in the Department for the Economy (DfE). The DfE publishes a description of the process for the award of Mineral Prospecting Licences (MPLs) and how to apply for licences to explore for and extract minerals and petroleum. DfE also consults publicly on applications, which are accepted on a “first come, first served” basis, although there is provision for a competitive process where there is more than one interest in an area. Information on mineral prospecting licences and applications and mining licences is currently available on the DFE website.

The Crown Estate and Crown Estate Scotland: marine environment

The Crown Estate manages the seabed to the 12-nautical mile territorial limit and other rights including non-energy mineral rights out to 200 nautical miles in all parts of the UK excluding Scottish territorials waters and the Scottish offshore zone, where Crown Estate Scotland manages these rights.

TCE typically awards, through a market-based tendering process, commercial agreements to companies to explore for or extract marine aggregate minerals, and it collects royalties for minerals extracted. All licensed application and exploration/option marine aggregate area details are published online and are available at no charge. TCE does not disclose contracts and agreements relating to minerals where they contain commercially confidential information.

Following the successful completion of the 2018 Marine Aggregates tender, and recent engagement with the sector, TCE intend to hold their next tender round during 2021/22. This tendering process will offer applicants the opportunity to seek rights for the exploration of aggregates (sand and gravel) lying on or under the seabed, in offshore areas of English and Welsh waters.

Pre-qualification will commence in the spring of 2021, with the Invitation to Tender stage (ITT) beginning in the summer. Following tender evaluation and assessment, and subject to the requirements of a plan-level Habitats Regulations Assessment, rights could be awarded at the end of the summer of 2022. Successful applicants would then be required to obtain all relevant statutory consents prior to the commencement of activities. Once the Exploration and Option Agreement is completed, information will be added to the TCE Open Data Portal, including the name of the applicant.

There are no currently commercial marine aggregate extraction licenses in Scotland, future proposals would lead to an equivalent process with the relevant seabed manager.

Such rights and options can only be exercised once the necessary regulatory consent (marine licence) is obtained under the Marine and Coastal Access Act 2009 or Marine (Scotland) Act 2010 from the national regulator – the Marine Management Organisation (MMO) in England, Natural Resources Wales (NRW) who administer the licensing regime on behalf of Welsh Government, Scottish Government Marine Directorate or in Northern Ireland the Department of Agriculture, Environment and Rural Affairs (DAERA) – according to location [8]. All regulators are required to keep a register available to the public of marine licences they have issued [9]. Applications for marine licences must be publicised to allow anyone who is interested an opportunity to make representations [10].

Revenue streams for marine aggregates comprise:

- Rent and production royalty payments to TCE [11].

The Marine Aggregates Capability and Portfolio report published by TCE provides a summary of the current aggregate extraction activity offshore, as well as remaining reserves on the seabed around England, Wales and Northern Ireland. Further details of reserves of primary marine aggregates by region are published in the Marine Aggregates Annual Review and Marine Aggregates - The Crown Estate Licences - Summary of Statistics. These two publications also include data on volume of exports to mainland Europe of material extracted from TCE licensed areas.

TCE also provides access to survey data and reports collected by offshore renewable and marine aggregates customers via their Marine Data Exchange and access to all data that they publish via their Open Data Portal.

The Crown Estate and Crown Estate Scotland: terrestrial minerals

TCE also grants mineral leases across England and Wales (except in Scotland) for land-based mineral extraction operations, including sand, gravel, hard rock, dimension stone and slate. It charges royalties for minerals extracted. Lease conditions and royalty payment provisions are negotiated on an open market and case-by-case basis. Crown Estate Scotland undertakes the same process for minerals on Scottish Crown Estate assets.

TCE also manages the right to gold and silver (“Mines Royal”) [12], in England and Wales, but there is no significant gold or silver production in these areas.

In Northern Ireland under the Mineral Development (Northern Ireland) Act 1969 with certain exceptions (exceptions include gold and silver) all mineral rights are vested in the Department for the Economy (DfE). Since 1970 the mineral rights specified in the 1969 Act are held in public ownership.

In Scotland, Crown Estate Scotland manages the rights to Mines Royal across most of Scotland. Planning permission was granted in Autumn 2018 for a gold mine at Cononish, Tyndrum. Crown Estate Scotland has granted lease rights to the operator for the extraction of gold and silver.

Local Planning Authorities (planning obligations payments)

Planning obligations are agreements made between a planning applicant (including the freehold owner of land where the operator only has a minerals lease) and a Local Planning Authority (LPA) (in their capacity as the mpa) under section 106 of the Town and Country Planning Act 1990 in England and Wales, section 75 of the Town and Country Planning (Scotland) Act 1997 (as amended by the Planning etc. (Scotland) Act 2006) in Scotland and Article 40 of the Planning (Northern Ireland) Order 1991. Planning obligation payments are site-specific and negotiated case by case. They may comprise:

- Monetary payments to LPAs; or

- “In-kind” infrastructure provisions: mainly off-site provisions, (on-site provisions within the boundary of a planning permission are theoretically possible but more likely to be included in planning conditions rather than under planning obligations).

The difference between off- and on-site “in-kind” infrastructure provisions can be understood as between provisions that benefit the local community and those used by the extractive company itself. Only monetary payments and off-site provisions are in scope for the UK EITI.

Planning obligations can be short term, such as obligations to carry out works before the extraction can take place, or long term, such as obligations to restore or provide after-care of extraction sites.

Obligations are generally recorded in online planning registries kept by LPAs, but payments owed or made are not always recorded, and no central registry of such planning obligations or relevant payments exists. In Scotland planning obligations are registered with the Registers of Scotland in order to be binding on successors in the event the ownership or operators of the land changes.

Environmental and social impact of extractive activities

Offshore mineral extraction (marine aggregates)

A Marine Licence from the appropriate licensing authority is required to remove any substance or object from the sea bed (e.g. mineral extraction) within the UK marine licensing area or the Scottish marine area (The Marine and Coastal Access Act 2009, The Marine (Scotland) Act 2010). Marine licence applications for mineral extraction are likely to require the submission of an Environmental Impact Assessment. The appropriate licensing authorities are the Marine Management Organisation in England, Natural Resources Wales in Wales, Scottish Government Marine Directorate in Scotland and the Department of Agriculture, Environment and Rural Affairs in Northern Ireland.

Onshore extraction of other minerals

Extraction of minerals is subject to the UK’s mineral planning process. The aim of mineral planning is to facilitate the sustainable supply and use of minerals. Mineral working is not a permanent use of land, and extraction sites are usually restored for beneficial after-use.

Mineral planning policy is devolved and set out in the National Planning Policy Framework (England), Planning Policy Wales and National Planning Framework 4 (Scotland). . In Northern Ireland, policy and guidance are provided through documents such as the Strategic Planning Policy Statement for Northern Ireland, which partly supersedes the Planning Strategy for Rural Northern Ireland. In Northern Ireland since 1 April 2015 responsibility for planning is shared between the Department of the Environment (from 8th May 2016 in respect of planning, the Department of Infrastructure and the eleven local councils).

Exploration for and extraction of metalliferous and industrial minerals are licensed by the Department for the Economy in Northern Ireland under the Mineral Development (Northern Ireland) Act 1969. The UK framework is supported by technical documents providing guidance on particular issues of mineral planning. The focus of the mineral planning process is on whether the development itself is an acceptable use of the land [1].

In England, mineral planning and decisions on planning applications are a responsibility of a local authority body referred to as mineral planning authorities (mpas). In most of England, mpas are the County Councils or National Parks. In Wales and Scotland, Local Planning Authorities including Local Authorities and National Parks Authorities are largely responsible for minerals planning. In Wales and some parts of England the mpa function may be delivered by Unitary Authorities. In Northern Ireland, the Minerals Unit, part of the Planning Service of the Department of the Environment, was responsible for minerals planning until 1 April 2015 [2].

Mpas/local planning authorities have four areas of planning responsibility:

- Planning to guide future developments;

- Safeguarding mineral resources;

- Managing developments by deciding on planning applications; and

- Monitoring and enforcement of existing planning permissions.

Some minerals permissions last for several decades, and where this is the case there may be a need for periodic reviews of the planning conditions attached to that permission. Mpas control mineral developments under the orders established under the Town and Country Planning Act 1990 (Section 97, Part II of Schedule 5, and Schedule 9) [3]. In Scotland, local planning authorities control mineral developments under the Town and Country Planning (Scotland) Act 1997, including Schedule 3.

Minerals extraction may only take place if the operator has the agreement of the landowner and has obtained both a planning permission from the mineral planning authority and any other regulatory permits and approvals.

Environmental and Social Impact Assessment (ESIA)

As part of the planning process for mines and quarries, Environmental and Social Impact Assessments (EIAs and SIAs) are generally required. These mean that a project's potential environmental and social impacts are evaluated systematically before it is implemented. They involve several key steps to ensure that adverse impacts are identified, mitigated and managed. The goal is to integrate environmental and social concerns into decision-making and minimize or avoid negative effects.

Control of Major Accident Hazards

The Control of Major Accident Hazards (COMAH) Regulations limit the consequences to people and the environment of any major accidents involving dangerous substances which occur. COMAH 2015 is enforced by a Competent Authority that comprises the Health and Safety Executive (or the Office for Nuclear Regulation for nuclear establishments), acting jointly with the appropriate environmental agency. In England this is the Environment Agency, in Wales it is Natural Resources Wales and in Scotland it is the Scottish Environment Protection Agency.

Fiscal regime

Mining and quarrying companies pay corporation tax (CT) on their profits at the standard rate, unlike profits from oil and gas extraction, which are subject to Ring Fence CT regime. Profits from upstream and downstream activities are not separated, and such companies pay a single amount of CT on the profits arising from all their activities. It is therefore not possible to say how much of the taxes paid by the companies whose tax payments are reported here related to their extractive activities nor what the total of such taxes was (and therefore what proportion of the total is covered by this report).

Companies based in the UK have to pay CT on all their taxable profits, wherever in the world those profits originate, although double taxation relief is available where appropriate to avoid the same profits being taxed twice. Companies not based in the UK, but with branches operating in the UK, have to pay CT on taxable profits arising from their UK activities. CT payments by mining and quarrying companies are included in the scope of the UK EITI. The figures reported are for total CT and include tax on both upstream and downstream activities. Corporation tax is paid by a small number of larger companies whose activities are primarily downstream.

Capital allowances are a feature of business taxation in the UK and apply to the mainstream CT regime (as well as to income tax). For CT purposes, the general rule is that capital expenditure is not allowed as a deduction for tax purposes. This means that profits chargeable to CT cannot be reduced by depreciation or similar expenses. The capital allowance regime exists to provide some relief for capital expenditure incurred. The main allowance which is commonly relevant for companies carrying on mining and quarrying activities is Mineral Extraction Allowance (MEA).

Research and Development Expenditure Credit (RDEC) is a tax credit available to companies operating in all sectors. It is generated by spend on research and development, and is claimed as a tax credit. There are a number of ways in which a company can receive payment of their RDEC claim, including offsetting against another of its tax liabilities and receiving a cash repayment. More information on RDEC can be found in HMRC guidance and statistics on RDEC can be found here. For EITI reporting purposes, tax payments/repayments are reported exclusive of any adjustment for RDEC.

There are several other payment streams, such as the Aggregates Levy, which involve payments from extractive companies to the Exchequer. These are outside the scope of EITI as they are indirect taxes not direct taxes. They are documented by the ONS in its annual publications on environmental accounts and environmental taxes [13].

Coal

Ahead of collection and publication of information on extractive-related payments to the UK government in 2018, the UK EITI Multi-Stakeholder Group decided to exclude such payments to the Mining Remediation Authority (formerly the Coal Authority). These payments are no longer material relative to overall government revenues and the MSG believes that their exclusion will not affect the comprehensiveness of UK EITI reporting. The continuing economic contribution of the coal sector is, though, still included in the background information set out below.

The Mining Remediation Authority is a regulatory executive non-departmental public body, established in 1994 when the industry was privatised. It is sponsored by the Department for Energy Security and Net Zero. The Authority owns, on behalf of the State, the majority of unworked coal and abandoned underground coal mine workings in GB and regulates and grants licences for working of coal and underground coal gasification (UCG), together with agreements to enter its coal estate for other processes such as coal bed methane extraction, abandoned mine methane extraction, mine water heat recovery and deep energy exploitation (e.g. geothermal, shale gas).

The Mining Remediation Authority holds an offline public registry of licences and does not publish licences online. Information about coal licences can be requested by post and email [14]. The Authority provides online coal mining data including on licence areas and known areas of activity.

Mining Remediation Authority revenue streams include:

- Fees for statutory licences, either operating or conditional (where the licensee is yet to secure planning permission) for surface and underground coal mining operations and UCG;

- Fees for licences for coal exploration;

- Production-related rents under coal leases which transfer the property interest in the coal to the licensee when holding an operating licence;

- Fees and royalties for digging and carrying away coal during non-coal-related development (Incidental Coal Agreement);

- Fees for agreements to access or pass through the Authority’s coal estate for processes such as coal bed methane and abandoned mine methane extraction, mine water heat recovery and deep energy exploitation (e.g. geothermal, shale gas); and

- Payments for coal rights under options for lease (granted with conditional licences) and rights for pillars of support in coal.

Further information on licensing activity can be obtained from the Mining Remediation Authority.

The majority of coal output comes from surface mining (opencast) sites in Scotland, North East England and South Wales. UK coal production peaked in 1913 and has been contracting, with fluctuations, since the mid-twentieth century, with the sharpest decline in the 1990s. Electricity-generating power stations currently account for most of the UK’s coal consumption.

| 2018 | 2019 | 2020 | 2021 | 2022 | |

| Volume (million tonnes) | |||||

| Deep-mined production | 0.02 | 0.10 | 0.11 | 0.09 | 0.06 |

| Surface-mined production | 2.76 | 2.49 | 1.57 | 0.96 | 0.59 |

| Total production | 2.78 | 2.59 | 1.67 | 1.05 | 0.65 |

| Gross Exports | 0.63 | 0.74 | 1.31 | 1.13 | 0.59 |

| Gross Imports | 10.08 | 6.23 | 4.53 | 4.61 | 6.36 |

| Net Exports | 9.45 | 5.49 | 3.22 | 3.48 | 5.77 |

| Value (£ million) | |||||

| UK production | 150 | 200 | 120 | 10 | 155 |

| Gross Exports | 85 | 90 | 100 | 120 | 170 |

| Gross Imports | 1,015 | 700 | 445 | 630 | 1,660 |

| Net Exports | 930 | 610 | 345 | 510 | 1,490 |

Source: Energy Trends Table 2.5 (DESNZ, October 2023) DUKES 2023 Table 1.2 (DESNZ, July 2023)

The data presented in Table 1 above are available on request from the UK EITI Secretariat.

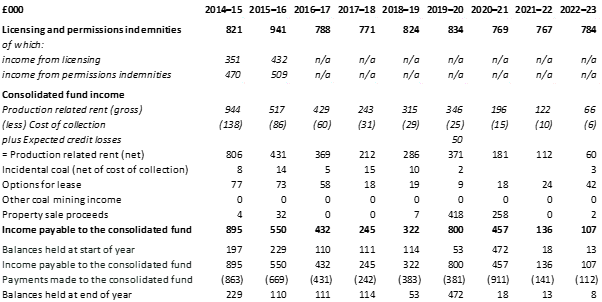

The Authority acts as an agent on behalf of the consolidated fund. Amounts collected and payable to the consolidated fund are reduced to cover the Authority’s cost of collection. This income adjustment is included within Licensing and permissions indemnities income given above.

Production related rent is earned on each tonne of coal extracted from existing operating coal mining sites. Incidental coal is royalty income from other sites where coal production is incidental to the main purpose of the activity being carried out.

Options for lease for future coal mining sites are granted in the form of a conditional licence and option for lease for the coal and income is recognised on the granting of the option. The site cannot become operational until certain conditions (for example, planning consent) have been met and payments are made annually based on the area of the option.

Property sale proceeds are recognised within the consolidated fund income where the initial purchase was made from grant in aid in previous periods. Income is recognised following the exchange of contracts and on completion of the sale of property.

Cost of collection relates to the element of income retained to finance licensing activities and the cost of any unrecoverable amounts owed.

Balances held at end of year represent amounts still to be remitted to the consolidated fund.

Table 2. Coal Authority Extractive Income as given in Mining Remediation Authority Annual Reports and Accounts

The Authority acts as an agent on behalf of the consolidated fund. Amounts collected and payable to the consolidated fund are reduced to cover the Coal Authority’s cost of collection. This income adjustment is included within Licensing and permissions indemnities income given above.

Production related rent is earned on each tonne of coal extracted from existing operating coal mining sites. Incidental coal is royalty income from other sites where coal production is incidental to the main purpose of the activity being carried out.

Options for lease for future coal mining sites are granted in the form of a conditional licence and option for lease for the coal and income is recognised on the granting of the option. The site cannot become operational until certain conditions (for example, planning consent) have been met and payments are made annually based on the area of the option.

Property sale proceeds are recognised within the consolidated fund income where the initial purchase was made from grant in aid in previous periods. Income is recognised following the exchange of contracts and on completion of the sale of property.

Cost of collection relates to the element of income retained to finance licensing activities and the cost of any unrecoverable amounts owed.

Balances held at end of year represent amounts still to be remitted to the consolidated fund.

Source: Coal Authority Annual Reports and Accounts (latest publication consulted, July 2023)

The data presented in Table 2 above are available on request from the UK EITI Secretariat.

Construction Minerals

Construction minerals include the extraction of igneous rock (including granite), limestone, dolomite and chalk for construction use, sandstone, sand & gravel, slate, gypsum, clay & shale and fireclay. Brick clay is an essential raw material for the manufacture of bricks; limestone and chalk are the primary materials for the production of cement.

These minerals are essential to the UK economy, improving our housing stock, transport networks, commercial and industrial buildings, energy and water infrastructure, schools and hospitals.

The main element of construction minerals in volume terms is the extraction of primary aggregates, including quarried crushed rock and both land-won and marine dredged gravel and sand. According to the Mineral Products Association, in 2022 the UK industry produced 191.1 million tonnes of primary aggregates, representing 2.5 times the total tonnage of energy minerals produced in the same year [15]. Within this, 135.1 million tonnes of crushed rock and 56 million tonnes of sand and gravel were produced.

Marine-dredged aggregates satisfied 14 million tonnes (25%) of the total construction needs for sand and gravel in 2022[16]. It also provides a strategic role in supplying large scale coast defence and beach replenishment projects - over 30 million tonnes being used for this purpose since the mid 1990's. With the growing threats posed by sea level rise and increased storminess, the use of marine sand and gravel to protect vulnerable communities and infrastructure around our coast will become increasingly important. In 2022, 1105 km2 of seabed was licensed for marine aggregate extraction in British waters, of which 107 km2 was dredged. This represents just 0.12% and 0.01% of the total UK continental shelf area (867,000km2) respectively [17].

Regionally most (67% of) UK primary aggregates production in 2022 took place in England, 14% in Scotland, 12% in Northern Ireland and 8% in Wales [18]. This includes both land-won and marine dredged aggregates.

Primary aggregates are largely extracted from indigenous sources and imports are limited, estimated to represent less than 5 million tonnes per annum. Small tonnages of crushed rock, marine sand & gravel, and dimension stone are also exported, mainly to Belgium, France and the Netherlands. Exports of UK construction aggregates were valued at £58.3 million in 2023, compared with imports worth £73.9 million [19].

The supply of primary aggregates is supplemented by the availability of recycled materials obtained from construction and demolition waste, as well as sources of secondary materials derived from other extractive and industrial activities and processes. Recycled aggregates are the product of processing inert construction and demolition waste, asphalt planings and used railway ballasts into construction aggregates. Secondary aggregates are derived from other industrial processes, such as other mineral extraction operations including ball and china clay production, or waste from slate and chalk production. Other sources of secondary materials include blast furnace and steel slags, incinerator bottom ash, furnace bottom ash, and coal-derived fly ash.

Whilst there have been some variations in the relative importance of the different sources of aggregates over the past 60 years, the contribution of recycled and secondary materials to total aggregates supply increased substantially since the early 1990s. Although there are no official statistics available on the contribution of these materials to the total aggregates market, the Mineral Products Association estimates that, in 2022, recycled and secondary sources of aggregates accounted for 30% of total aggregates supply in Great Britain, significantly higher than the European average [20].

The underlying geology across the UK determines the local availability of construction minerals and aggregates (especially crushed rock) may be transported long distances when necessary. The South East, for example, has its own supplies of sand & gravel alongside recycled aggregates, but relies heavily on crushed rock brought in by rail from the East Midlands and the South West of England. It also uses marine dredged sand & gravel from coastal waters and landed at wharves in south coast ports and along the Thames river [21].

Market drivers for construction minerals include general UK economic and construction growth. In recent years, the aggregates market has experienced significant volatility. After a decline in 2020 due to the pandemic, there was a rapid recovery in construction demand for aggregates in 2021. However, in 2022, demand started to slow, due to the knock-on effects of a wider economic and construction slowdown caused by global supply chain bottlenecks post-pandemic and the war in Ukraine. Rising inflation, higher interest rates and sub inflation wages growth have led to the largest drop in living standards in decades, impacting household spending, business investment and general confidence in the economy. For construction, increasing reports of projects delays, descoping and outright cancellations caused by cost pressures and wider economic uncertainties have put pressure on minerals and mineral products markets, including aggregates. Aggregates sales volumes in Great Britain declined for two consecutive years in 2022 and 2023, with volumes down 12.8% in 2023 compared to 2021 [22]. Contrasting with short-term weaknesses in the outlook, the long-term prospects for the aggregates markets remain positive, with substantial construction demand expected over the next 15 years to deliver the green growth agenda, including the energy transition and Net Zero [23].

The construction aggregates sector is a significant source of local employment, particularly in rural areas, and contributes to sustainable material supply due to abundant local resources and low imports.

Whilst there are sufficient indigenous mineral resources available to support future demand requirements, a key factor influencing the future, long term supply of aggregates, and therefore other mineral products manufactured using aggregates, is the operation of the mineral planning system. Permitted reserves of aggregates have been declining over the past 20 years, with sales consistently outpacing the tonnage of new reserves granted [24]. This decline is unsustainable and may lead to future local supply shortages at a time when as green growth policy initiatives will require increasing volume of aggregates to be supplied for the construction and maintenance of upgraded infrastructure and buildings. While recycled and secondary sources of aggregates supply will help support our construction needs, primary aggregates are still expected to fulfil the majority of demand for the next 15 years [25].

Construction minerals extraction and related downstream manufacturing activities are distributed throughout the UK and extraction businesses make a variety of tax, financial and non-financial contributions to national and local governments and local communities that are outside the current scope of EITI reporting. This includes the Aggregates Levy, employment taxes and businesses rates. The aggregates industry also supports a significant supply chain of plant, equipment and transport suppliers and professional services. Other construction-related mineral extraction includes clay for brick-making, limestone and chalk for cement manufacture and the production of high-quality dimension stone and slate.

At the extraction stage, the UK Aggregates Levy was introduced in 2002 as an environmental tax with the aim to encourage recycling and use of by-products from other industrial processes. The rate was initially set at £1.60 per tonne, increased to £1.95 per tonne in 2008 and £2.00 per tonne in 2009, and has since remained frozen. In 2022, the annual cost of the Aggregates Levy reached £378m in 2022 [26].

The UK-wide Aggregates Levy currently applies in Scotland, but the Scotland Act 2016 gives the Scottish Parliament the power to introduce a devolved levy. The Scottish government's Aggregates Tax Bill is currently at the final stage and will replace the existing UK-wide levy in due course. There is no clarity yet as to the rate it will be levied at, although the design of the tax has stayed very close to the UK levy it will replace.

Further down the supply chain, elements of the mineral products industry, such as cement and lime manufacture, also fall within the scope of the UK Emissions Trading System, Climate Change Agreements, Streamlined Energy and Carbon Reporting and Energy Saving Opportunity Scheme, all of which are focused on carbon reduction or energy efficiency.

The UK Government has committed to deliver Net Zero emissions by 2050.

The extraction of minerals, their processing and transport to market generate carbon emissions, the quantum of which will depend on the material considered, the method of extraction used and the transport required. Based on 2016 data, a WWF report [27] identified that carbon emissions from “Other mining and quarrying product”’ (i.e. non-energy and metals extraction) activities represented just 0.2% of total UK production emissions, and stood 46% below levels of emissions in 1990.

Focusing on construction aggregates, the increasing contribution of low carbon energy in the mix have resulted in lower carbon emissions per tonne of crushed rock and sand & gravel on-site production in recent years, which stood at 3.0 kg/tonne and 2.7 kg/ tonne respectively in 2020, excluding the carbon cost of transporting products to their point of use [28]. Site management and restoration also play an important role in the delivery of national and local biodiversity targets and objectives, including net gain and nature recovery, as well as for adaptation to the effects of climate change.

In the wider mineral industry supply chain, the UK concrete and cement sector set out in 2020 a roadmap to become net negative by 2050, removing more carbon dioxide from the atmosphere than it emits each year [29]. A roadmap to net negative by 2040 was also published in 2023 for the lime sector [30].

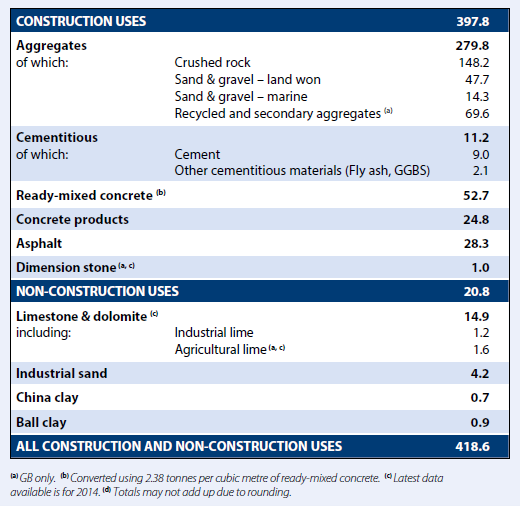

Further detailed information on the extraction and manufacturing of non-energy and non-metals minerals and mineral products is available on table 3. A total of 419 million tonnes of essential aggregates, industrial minerals and other manufactured mineral products were produced in Great Britain in 2021.

Other data can also be found from the British Geological Survey (BGS) Minerals Yearbook.

Table 3 Minerals and Mineral Product Sales in Great Britain, 2021 (million tonnes)

Source: Profile of the UK Mineral Products Industry - 2023 Edition (2023)

Permitted reserves of land-based primary aggregates by region are provided in the 4 yearly Aggregate Minerals surveys for England and Wales prepared by the British Geological Survey (BGS).

Other data can also be found in the British Geological Survey (BGS) Minerals Yearbook.

The Department for Business and Trade (DBT) publishes quarterly and annual data on the value of EU and Non-Eu (imports and exports) for selected construction materials, including aggregates and other mineral products.

Industrial Minerals

Please note that not all final production figures for 2020 for industrial minerals are available yet.

Industrial minerals include a number of raw materials used in specialised processes, with notable production in the UK of the following [31].

Kaolin - Kaolin, also known as china clay, is a commercial clay with specialist applications in paper production, ceramics, cosmetics and other industries. UK deposits of kaolin are concentrated in Cornwall and Devon and are world-class in terms of size and quality [32].

Production peaked in 1988 at 2.8 million tonnes but since then has declined to an estimated 709 thousand tonnes in 2022, 90% of which was exported, mostly to Europe.

Ball clay - Ball clay, another major industrial mineral, is produced in Devon and Dorset mainly for the manufacture of white ware ceramics. Production levels peaked between 2005 and 2008 at more than 1 million tonnes. In 2022, production was estimated at 1,040 thousand tonnes and exports reached 527,551 tonnes.

Production of potash (a processed product also known as muriate of potash, or MOP) has now ceased and has been replaced by polyhalite, an unprocessed mixture of potassium minerals. Production of polyhalite was 953,000 tonnes in 2022.

Yorkshire has one of the largest proven world deposits of potassium-rich minerals. There is one potash mine in the UK, at Boulby, Yorkshire, which currently produces approximately 1 million tonnes per year of polyhalite and directly employs 1,000 people, half of whom work underground [33],

In June 2015 a planning application was approved for another mine in the North York Moors (NYM) National Park.

The Woodsmith Mine, an Anglo-American project, currently in development is the UK’s biggest underground mining project for many years. Based in North Yorkshire it will mine, process and supply polyhalite an organic crop fertiliser.

Salt - England accounts for 95% of UK salt production, 80% of which takes place in Cheshire; the Boulby potash mine in Yorkshire is another large centre. About 70% of salt is extracted through solution mining, the rest mined as rock. County Antrim is the main area of salt production in Northern Ireland. Rock salt is primarily used for de-icing roads and in agriculture. Brine salt is chiefly used in chemical industrial processes that require chlorine. An estimated 2.312 million tonnes of salt were produced in the UK in 2020 with exports estimated at 374,671 tonnes. The Winsford Salt mine, an underground mine in Cheshire, produces rock salt for road treatment in winter.

Silica sands contain a high proportion of silica and their properties make them essential for glass making, foundry work and a wide range of other industrial and horticultural applications. UK production has declined from approaching 7 million tonnes in 1974 to an estimated 4.9 million tonnes in 2022. Exports were estimated to be 118,779 tonnes in 2021.

Gypsum - Natural gypsum is used in plaster, plasterboard and cement making and has historically been mainly extracted by mining in the UK. The amount extracted in the UK has declined appreciably because of the use of desulphogypsum derived from flue gas desulphurisation at coal-fired power stations. In 2022 the UK produced an estimated 2.4 million tonnes, with exports of 21,126 tonnes.

British Gypsum operates 5 sites throughout the UK extracting gypsum for the production of plaster and plasterboards.

Industrial and agricultural carbonates are important in iron and steel making, sugar refining and glass making, as fillers in various products, to reduce soil acidity in agriculture, and for flue gas desulphurisation in coal fired power generation. Total industrial carbonates production peaked at around 11.5 million tonnes in the late 1990s but was around 9 million tonnes in 2014.

Fluorspar is the most important and only UK source of the element fluorine, most of which is used in the manufacture of hydrofluoric acid. It is extracted from the Southern Pennine ore field in the Peak District National Park. In 2022, an estimated 13,000 tonnes were extracted, with exports estimated to be 15,053 tonnes.

British Fluorspar operates one underground mine in the Peak District and undertaking studies as to reopen an older operation. Mines and processes acid grade fluorspar a key raw material for the production of hydrofluoric acid, fluorocarbons, fluoropolymers and aluminium fluoride. These chemicals are used in a variety of industries such as the automotive, electronic, construction and chemical industries as well as in the production of aluminium and steel.

Barytes is principally used as a weighting agent in drilling fluids used in hydrocarbon exploration, to which its fortunes have been linked. The major source comes from the Foss mine near Aberfeldy in Scotland. Production in 2022 was estimated to be 30,000 tonnes. Exports for 2020 amounted to 13,221 tonnes.

M-I SWACO operates one underground mine (Foss Mine) in Scotland and developing a second mine (Dunanlich) producing barytes mainly used in the oil and gas industry in drilling fluids.

Metal Minerals

Tungsten (wolfram) is an essential element in a range of industrial processes, valued for its high melting point, density and extreme strength. England hosts the world’s fourth largest known tungsten deposit – the Drakelands Mine near Plympton, Devon.

This has been estimated to contain 318,800 tonnes of tungsten metal, or about 10% of the world’s known reserves, as well as an estimated 43,700 tonnes of tin. Production at Drakelands, historically known as Hemerdon mine, began in 2015 after a 70-year break, operated by Australian company Wolf Minerals, but stopped in 2018 following the operating company going into administration [34].

In 2018 production of tungsten was estimated to be 1,240 tonnes in the UK, with exports estimated to be in the region of 1,507 tonnes in 2020 (including scrap, unwrought, wrought, carbide and ferro-tungsten).

The above data are sourced from the BGS MineralsUK website and United Kingdom Minerals Yearbook 2023 publication and cover extraction from 2016–2022.

Please note that under the UK EITI Open Data policy users can re-use the data in the tables and figures.

- For environmental issues that may be considered during the planning process, see DCLG, Assessing environmental impacts from minerals extraction

- The functions of the Department’s Strategic Planning Division Minerals Unit in Northern Ireland transferred to each of the 11 councils on 1 April 2015. Under the 2-tier planning system, councils are the determining planning authority for the vast majority of planning application, including mineral applications. Applications of regional significance are submitted directly to the Department of the Environment. However, from 2016, applications in respect of planning should be submitted to the Department of Infrastructure under the provision set out in section 26 of the Planning Act (Northern Ireland) 2011.

- For more information see DCLG, Minerals planning orders

- The Crown Estate is an incorporated public body that manages the monarch’s property portfolio.

- Marine planning in England

Marine planning in Wales

Marine planning in Scotland

Marine planning in Northern Ireland - BGS Minerals UK, Legislation & policy: mineral ownership

- Mineral Development (Northern Ireland) Act 1969

- British Marine Aggregate Producers Association (BMAPA), Licensing and regulation; the Marine Management Organisation (MMO) is an executive non-departmental public body sponsored by the Department for Environment, Food & Rural Affairs

- England: MMO Public Register

Wales: Applications received and determined

Scotland: Marine licensing register

Northern Ireland: the functions and services delivered by Department of the Environment have been transferred to new Northern Ireland departments. A register of licensing information is available for inspection at all reasonable times by members of the public free of charge. Contact Marine Strategy and Licensing Branch or the Northern Ireland Environment Agency (NIEA), Marine Dredging. - UK Environmental Law Association, Marine Licensing

- Royalty rates vary between licences and are commercially confidential. Companies also pay “dead rent”, a standard minimum annual fee payable to TCE if no dredging has occurred within the past 12 months.

- With an exception of a few places in Scotland, where mineral rights were transferred historically.

- ONS. UK environmental accounts 2018

ONS. UK environmental accounts: environmental taxes

HMRC guidance, Environmental taxes, reliefs and schemes for businesses and, in particular, Excise Notice AGL1: Aggregates Levy - Contact details. Information about coal licences (including licensee details) can be viewed free of charge from the Coal Authority offices, but there is a charge if a copy is requested. Discussions are ongoing to set up an on-line electronic register.

- MPA. Profile of the UK Minerals Industry - 2023 Edition. Website: Mineral Products Association, 2023.

- The Crown Estate. Marine Aggregates - The Crown Estate Licences: Summary of Statistics. Website: The Crown Estate.

- MPA: Marine Aggregates.

- Profile of the UK Mineral Products Industry - 2023 Edition (2023).

- DBT. Building materials and components statistics: June 2024. Website: Department for Business and Trade, 2023. Statistics and analysis on the construction sector for June 2024.

- MPA. The contribution of Recycled and Secondary Materials to Total Aggregates Supply in Great Britain - 2022 Estimates. Website: Mineral Products Association, 2024.

- Mineral Products in London - Safeguarding London's Wharves and Rail Depots for future Prosperity and Sustainability. Website: Mineral Products Association, 2017.

- Quarterly Sales Volumes Survey. Mineral Products Association. (online) 2023. Industry survey of MPA producer members. http://www.mineralproducts.org/Facts-and-Figures/Quarterly-Sales-Volumes-Survey.aspx.

- Aggregates demand and supply in Great Britain: Scenarios for 2035. Website: Mineral Products Association 2022.

- AMPS 2022 - 10th Annual Mineral Planning Survey Report. Website: Mineral Products Association, 2023.

- Aggregates demand and supply in Great Britain: Scenarios for 2035. Website: Mineral Products Association 2022.

- HMRC. Environmental Taxes Bulletin. Website: HM revenue & Customs, 2023. Statistics on the Aggregates Levy (AGL).

- WWF. Carbon Footprint - Exploring the UK's contribution to climate change. Website: WWF UK, 2020.

- MPA. MPA Sustainable Development Report 2020/21. Website: Mineral Products Association, 2021.

- UK Concrete and Cement Industry Roadmap to Net Zero. Website: MPA UK Concrete, 2020.

- Net Negative 2040 Roadmap. Website: MPA Lime, 2023. Lime is part of the Mineral Products Association (MPA).

- Sources of data in this sub-section include: BGS, UK Minerals Yearbook, BGS, Mineral Planning Factsheets, BGS, UK mineral statistics, UK Minerals Forum, Trends in UK Production of Minerals

- BGS, Mineral Planning Factsheet, Kaolin

- BBC. Sirius minerals

- BBC. Wolf Minerals miners’ jobs at risk as it stops trading

| Abbreviation | Explanation |

|---|---|

| BEIS | Department for Business, Energy and Industrial Strategy |

| BGS | Department for Business, Energy and Industrial Strategy |

| BIS | Department for Business, Innovation and Skills |

| BMAPA | British Marine Aggregate Producers Association |

| CES | Crown Estate Scotland |

| CT | Corporation Tax |

| CNS | Central North Sea |

| CT | Corporation Tax |

| DAERA | Department of Agriculture, Environment and Rural Affairs |

| DCLG | Department for Communities and Local Government |

| DfE | Department for the Economy |

| EU | European Union |

| HSE | Health and Safety Executive |

| HSENI | Health and Safety Executive for Northern Ireland |

| GB | Great Britain |

| GDP | Gross Domestic Product |

| GVA | Gross Value Added |

| LPA | Local Planning Authority |

| MEA | Mineral Extraction Allowance |

| MMO | Marine Management Organisation |

| MPA | Mineral Products Association / Mineral Planning Authority |

| MPL | Mineral Prospecting Licence |

| MSG | Multi-Stakeholder Group |

| NIEA | Northern Ireland Environment Agency |

| NRW | Natural Resources Wales |

| NYM | North York Moors |

| ONS | Office for National Statistics |

| SEPA | Scottish Environment Protection Agency |

| TCE | The Crown Estate |

| UCG | Underground Coal Gasification |

| UK | United Kingdom |